Hey there, my friend! If you are sitting at your desk wondering why on earth you should pay a premium for smart cards when cheap traditional plastic cards are right there, you are not alone. Let’s dive into why smart cards cost more upfront, why global buyers are making the switch, and how they actually save you a fortune in the long run.

The Short Answer: Smart Card vs Traditional Card ROI

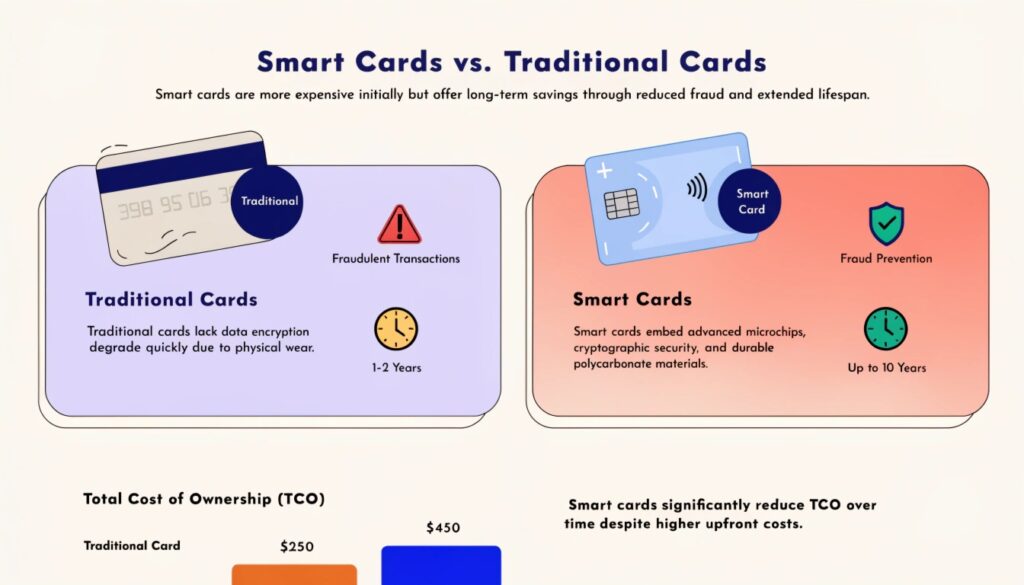

Smart cards are more expensive because they embed advanced microchips, cryptographic security, and durable polycarbonate materials. However, they stop fraud and last up to 10 years. Traditional cards lack data encryption and degrade quickly, meaning smart cards significantly reduce the total cost of ownership (TCO) over time.

Read on to see the real math behind B2B procurement and why relying on outdated traditional cards might be the most expensive mistake your organization makes this year.

Why Do Smart Cards Cost More Upfront?

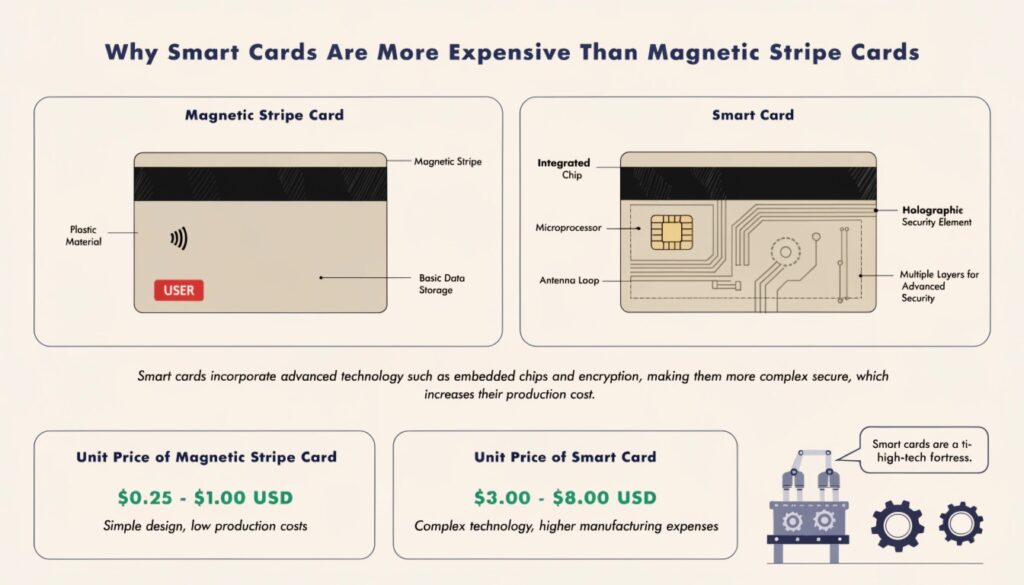

Let’s be real. When you look at a procurement quote, the unit price of a smart card can make you blink twice compared to a simple magnetic stripe card. But as an old friend in the security printing industry, let me pull back the curtain on why that price tag exists. It’s not just plastic; it’s a tiny, high-tech fortress.

The High Cost of Silicon and Encryption Technology

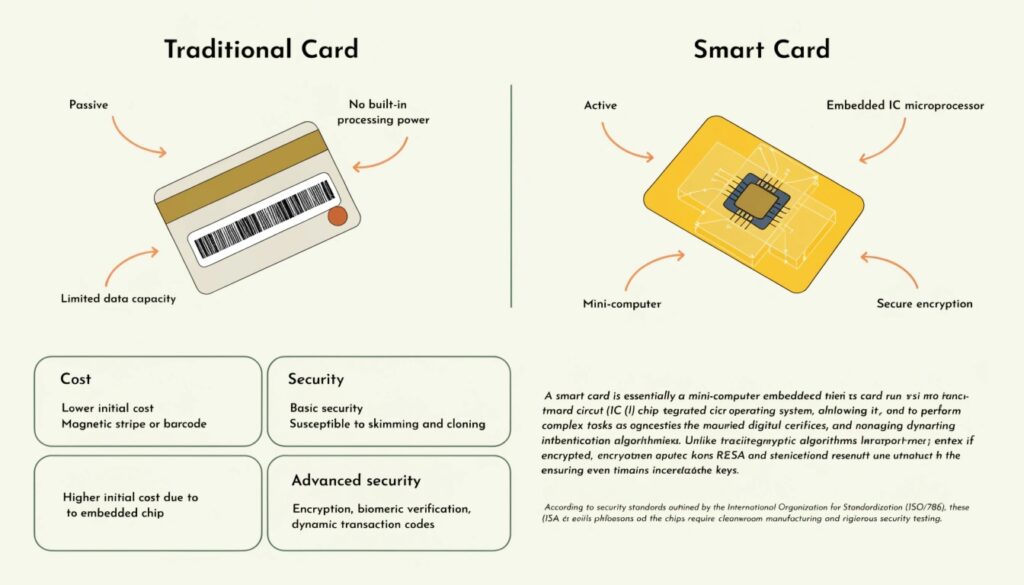

Traditional cards are essentially passive pieces of PVC with a magnetic strip or a printed barcode. They don’t “think.” A smart card, however, contains an embedded integrated circuit (IC) microprocessor.

This tiny chip runs its own mini-operating system and utilizes advanced cryptographic algorithms (like AES and RSA) to encrypt data. You aren’t just buying a card; you are buying a secure computing device. According to security standards outlined by the International Organization for Standardization (ISO/IEC 7816), these chips require cleanroom manufacturing and rigorous security testing, which naturally drives up the initial production cost.

Premium Materials: PVC vs Polycarbonate (PC)

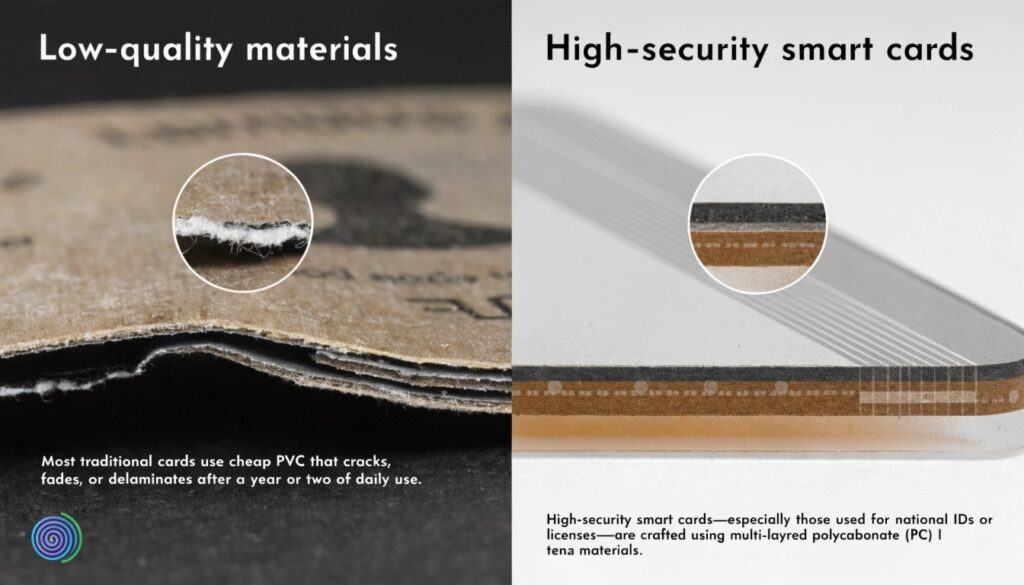

Most traditional cards use cheap PVC that cracks, fades, or delaminates after a year or two of daily use. High-security smart cards—especially those used for national IDs or driver’s licenses—are crafted using multi-layered polycarbonate (PC) materials.

When these layers are fused together under heat and pressure, they form a solid, tamper-evident structure that cannot be separated without destroying the card. This advanced material science ensures the card can withstand extreme wear and tear for over a decade.

+------------------------+-----------------------------------+-----------------------------------+

| Feature | Traditional Card (Magstripe/PVC) | Smart Card (Chip/Polycarbonate) |

+------------------------+-----------------------------------+-----------------------------------+

| Upfront Unit Cost | Extremely Low | Moderate to High |

| Average Lifespan | 1–2 Years | 5–10 Years |

| Security Level | Low (Easy to clone & skim) | Extremely High (Encrypted crypto) |

| Counterfeit Risk | High | Near Zero |

| Long-term ROI | Poor (Frequent replacements) | Excellent (Low TCO) |

+------------------------+-----------------------------------+-----------------------------------+

The Long-Term Math: Does the Average Cost Actually Decrease?

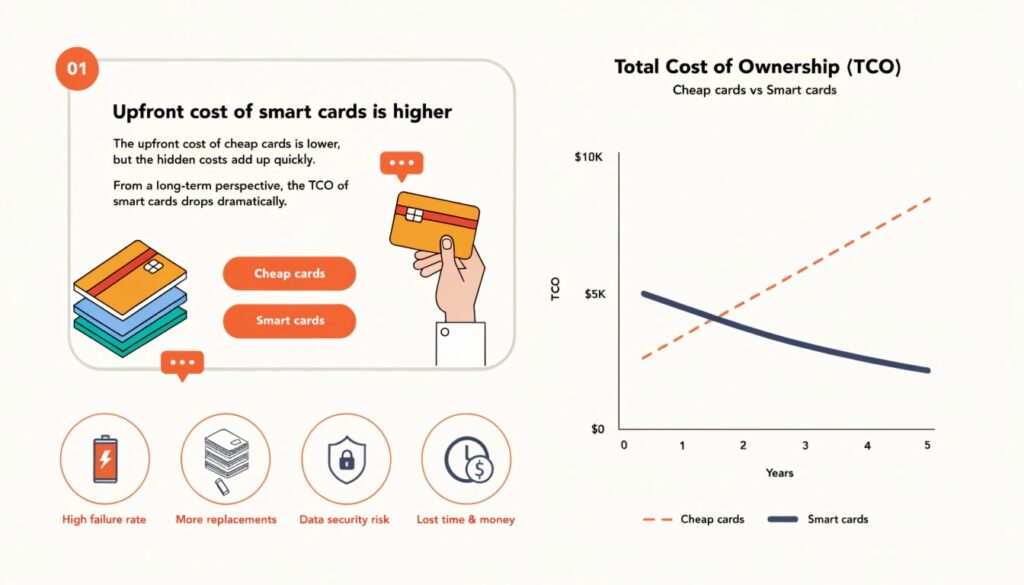

Now, let’s talk about the big breakthrough that will make your finance department smile. Yes, the upfront cost of smart cards is higher. But from a long-term perspective, the Total Cost of Ownership (TCO) drops dramatically. Let’s break down the hidden costs of “cheap” cards.

The Replacement Cycle Nightmare

Imagine you are procuring 100,000 ID cards for an organization.

- If you choose cheap traditional PVC cards, you will likely need to replace them every 12 to 18 months due to scratched magnetic stripes, broken plastic, or worn-out printing. Over 10 years, that is 5 to 7 rounds of complete re-issuance.

- If you invest in high-quality smart cards, a single card can easily last 10 years.

When you calculate the labor cost of re-issuing cards, shipping fees, and administrative hassle, the long-term average cost per year of smart cards is often much lower than traditional cards.

The Astronomical Cost of Data Breaches and Fraud

Here is the kicker: traditional cards are a goldmine for counterfeiters. Magnetic stripes can be skimmed and cloned in seconds using cheap hardware available online. According to global fraud reports compiled by organizations like The Nilson Report, global card fraud losses continue to cost billions of dollars annually.

If a hacker clones an employee access card or a government-issued credential, the resulting data breach or security failure can cost your organization millions. Smart cards use dynamic data authentication, making them virtually impossible to clone. The prevention of just one fraud incident pays for the entire smart card upgrade instantly.

Why Global B2B Buyers Superficially Choose Smart Cards

If you look at modern global procurement trends, international B2B buyers, governments, and financial institutions are completely abandoning plain plastic cards. Why? Because the market demands trust, multi-functionality, and future-proof technology.

Multi-Application Integration (All-in-One)

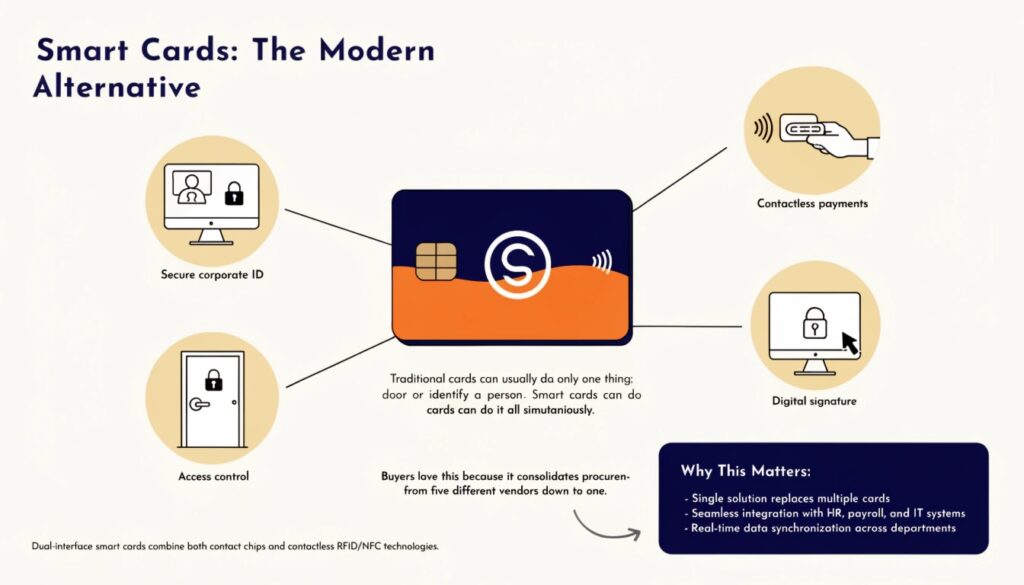

Traditional cards can usually do only one thing: open a door or identify a person. Smart cards can do it all simultaneously. Thanks to dual-interface technology (combining contact chips and contactless RFID/NFC), a single smart card can serve as a secure corporate ID, a contactless payment method, an access control token for secure areas, and a digital signature key for logging into company computers. Buyers love this because it consolidates procurement from five different vendors down to one.

Compliance with International Security Regulations

Today, industries worldwide face strict data protection laws. Whether it’s financial compliance or government identity security, organizations must meet stringent standards. High-security smart cards align perfectly with frameworks like the EMVCo standards for payment infrastructure and international biometric passport regulations. Buying smart cards isn’t just a tech upgrade; it’s a mandatory step for legal and operational compliance.

Summary: A Smart Investment for Your Brand

To wrap it all up, my friend: traditional cards are cheap today but incredibly expensive tomorrow. Investing in smart cards means you are paying for unbreachable security, a decade of durability, and a multi-functional ecosystem that streamlines your entire operation. When you look at the total lifecycle, smart cards aren’t an expense—they are an institutional cost-saver.